Beyond Flower

A Global Lens on Medical Cannabis—and the Company Built for the Coming Moment

(by me and my ChatGPT)

Disclosure: I am a shareholder of Avicanna. This is not investment advice. Please do your own due diligence.

Yelling at the Screen

The other day I was watching an interview between a prominent cannabis investor and a representative of the investee. I always appreciate investors and companies sharing their ideas openly, but at times I find myself yelling at the screen.

A recurring theme of my interview-watching discontent in the cannabis industry has to do with how many investors seem to know about one company or a small handful only and have not surveyed the competition thoroughly to understand what else is out there in terms of capabilities, products, margins, intellectual property, etc., particularly around the world.

I asked ChatGPT for the right adjective to describe this approach to company analysis. It gave me ‘parochial.’ It suggested ‘insular,’ ‘myopic,’ ‘context-blind,’ as well as ‘closed system thinking.’

Subsequently, the interview appears to have been scrubbed from the Internet. The direct topic of the interview and whatever may have been controversial are largely tangential to the points that I want to spotlight in this post, so I left the names out.

Framework and context, informs portfolios

The framework articulated by this investor about investing in the cannabis business sounded much like my own, but my portfolio probably couldn’t look any more different from what I know of his top holdings.

As they say, I am often wrong, but rarely in doubt, but my take when listening to many cannabis investors is that the context for understanding is limited by geography and exposure, and this, therefore, impacts interpretation of what they think they know.

This is a post about Avicanna, not another investor (who will remain anonymous out of respect for the scrubbed interview content) or another company, so I will try not to digress in those directions.

Nevertheless, I resonate to this quote from the interview, which certainly runs counter to conventional cannabis investing wisdom still:

“I’ve generally focused more on where the competition is most intense, because it’s my belief that if you can compete and succeed there, and you can figure out ways to win there, then you can win everywhere.”

That kind of environment in cannabis has tended to produce a certain type of operator. The past several years in cannabis have been difficult, with no capital availability, widespread losses, and very little margin for error. The companies that made it through are, almost by definition, scrappy survivors—forced to become disciplined, flexible, and efficient simply to stay alive. Those traits show up most clearly in cost structure, product consistency, customer/demand focus, execution and ultimately, ROIC.

The investor also spoke about how the future of the industry is about “cost” and “efficiency.” He talked about the “end state,” when competition is global and interstate restrictions are gone. He emphasized the need for a crystal clear, pure supply chain as markets become more medical and more export driven. In his post, he argued that only a small percentage of farms can consistently produce clean biomass and that this will matter enormously as vapes and medical markets grow. In the interview, he said, “the future increasingly looks more medical… you’ll have a rec market, but the medical seems to be the real opportunity.”

I agree with all of that, for the most part.

These same ideas have also shaped my own thinking over the last several years but my interpretation of them has evolved along with my exposure, which is a large part of why my cannabis portfolio has changed so much since I first arrived (when I too had a much narrower focus on the U.S. public markets and very little understanding of what was happening elsewhere).

Part of my perspective on investing in the cannabis industry is that we are in the very early stages of a fledgling, global industry that I believe can grow strongly perhaps for decades. As we’ve seen, that rising tide will not lift all ships, however, there’s an emergent pattern that appears in nature and other complex adaptive systems called preferential attachment. It’s the benefit a brand or company hopes to get from first-mover advantage, but in this industry, first-mover is a fools errand. In Cannabis, it is more like operating survivor with the best gross margins (which means IP) and the lowest costs.

If I can identify one of these future global leaders (as I certainly believe I have - as articulated elsewhere - with Auxly and here too with Avicanna), that is where the potential for a generational-type opportunity arises.

As a former retail analyst, I’ve been laser-focused on trying to find asymmetric opportunities, over years or decades, like I studied, witnessed and lived through with so many great retail growth stories including WMT, TGT, HD, LOW, GPS, LTD, COST, BBY, et al.

In cannabis, this means (IMO) intellectual property in the conventional sense, but also in the sense of expertise at scale that has been iterated over the course of years and gives a small handful of companies (eg Auxly) an important lead (IMO) in the race to preferential attachment, i.e. dominance. The potential for the transformation from the ‘babiests of the bathwater’ in coming years to the most profitable, recognized cannabis companies in the world is the wave I’m hoping to ride.

The Emerging Context

The broader the picture that emerged over time, the less any of what was happening cannabis-wise in the US was of interest to me.

Once I understood:

- the need for low cost, high quality, consistent cannabis at scale

- the recognition that the market will rationalize as low-cost supply emerges globally

- the relevance of brand in the ROIC equation

- the idea that this is already becoming a global market

- the recognition that medical cannabis provides more protected opportunity in flower relative to rec

- and the possibility that more advanced medical products may eventually inform pharmaceutical development

then I increasingly understood Avicanna as a collection of valuable assets (and, therefore, future cash flows), and the seeming silliness of its low (now US$15 million) market cap given how unique and important their platform appears to be on a global scale at this early point in the development of global medical cannabis.

Unlike cannabis investors I observe, my approach is more in the direction of trying to survey the landscape. How can I proclaim something as special unless I know what to compare it to? It took a long time to stop finding public companies that I had never heard of, but I think I have some sense of most of them at this point. The private landscape is much more difficult to assess in this manner, but I have been on the lookout for some time without getting a remarkable number of hits.

While there are a number of companies working on cannabinoid drug development, and others focused on medical cannabis, low-cost cultivation, or alternative delivery formats, they tend to exist in isolation. These businesses are relatively scarce, often capital constrained, and generally lack the integration that allows different parts of the system to reinforce one another.

There may be companies with meaningful intellectual property in areas such as cannabinoid formulations, drug delivery, or finished medical products. There are also platforms that touch pieces of the patient, physician, or distribution layer. But it is rare to see those elements brought together in a way that creates interaction between supply, product development, and real-world use.

That is what stands out here. The combination of global supply, medical infrastructure, proprietary formulations, and patient interaction begins to look less like a collection of assets and more like a self-reinforcing system that can continue to generate and refine its own intellectual property over time.

I do not believe there is another company in the world that brings those pieces together in this synergistic way. As it stands, this appears to be a unique asset that is in exactly the right place at the right time on its 10th birthday, after many years of unrelenting bad news and hard work.

I’ve been trying to follow the global goings on in medical cannabis as closely as I can from here in Marina del Rey, California and my sense as I assess the German and Australian markets and their evolution, the goings on in France and Switzerland, Poland, the UK and rumblings in many other countries, I believe medical cannabis is marching forward, and it is my sense that every market is ready for the Avicanna approach – beyond flower.

Beyond Flower

From my perspective an investor with a global context and a framework like that should see how the world is and understand why everyone will soon be looking for what Avicanna has to offer, regardless of how low it’s market cap happens to be today. Avicanna Is *the one and only* company (?) that combines low cost supply, medical infrastructure, proprietary formulations, real world patient interaction, and pharmaceutical optionality. This is the model for the moment IMO. And it all happens to be inside a market capitalization that is difficult to reconcile with the asset mix in the context I believe I see.

Medical Cannabis

If the future is global, if the future is medical, and if the future requires clean, consistent supply, then the real question is not simply who can produce compliant cannabis.

It is who can produce it at the lowest cost, at scale, and to a standard that can actually serve those markets.

And, as importantly - perhaps more - who has the customers and relationships to place that supply where it needs to go.

Those are not U.S. questions. They are global questions.

Canada has already offered important clues about market development, oversupply, pricing, margin compression, product iteration, medical infrastructure, and operating discipline. The global future will not look exactly like Canada, but Canada has still been one of the clearest laboratories for what this industry becomes after the flood.

That is the context in which I see Avicanna.

Why Avicanna

My story is about a little Canadian medical cannabis company with a TINY market cap, called Avicanna.

Avicanna emerges from the IP and interactions of its 4 business units. As each business unit becomes more global, they will increasingly overlap and form a global, vertically integrated, medical cannabis, self-reinforcing IP system.

The foundations have been laid over the last 10 years of entrepreneurship, boom and bust, capital starvation, scrappiness, pivots, network weaving and development by a devoted, hard-working team of experienced professionals.

At a high level, Avicanna consists of four business units. I am presenting them in the wrong order only for the sake of my narrative:

1. Santa Marta Golden Hemp (SMGH), its Colombian cultivation, extraction, and cannabinoid API platform

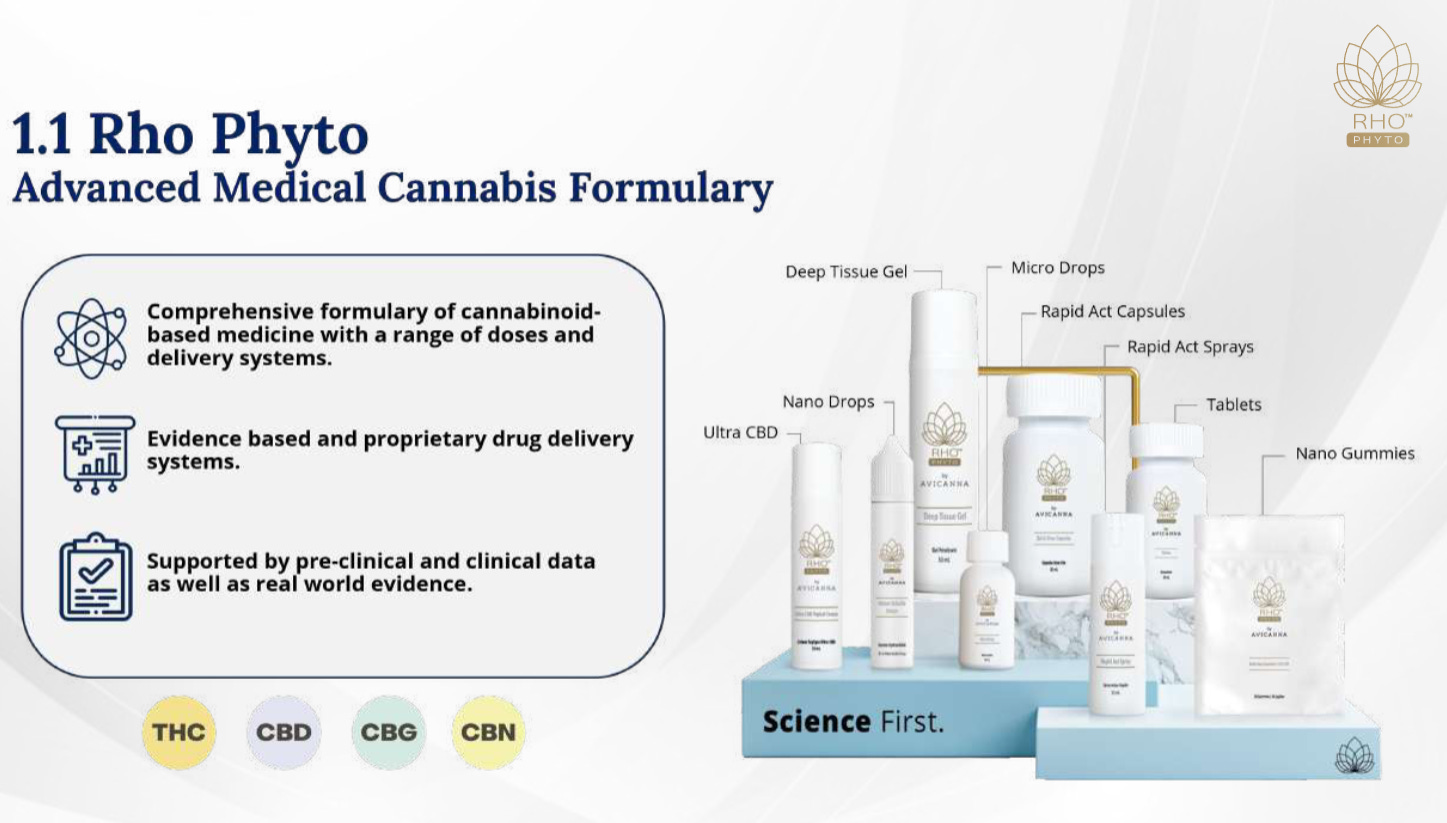

2. Rho Phyto, a portfolio of non-inhaled and standardized medical cannabis products and proprietary formulations

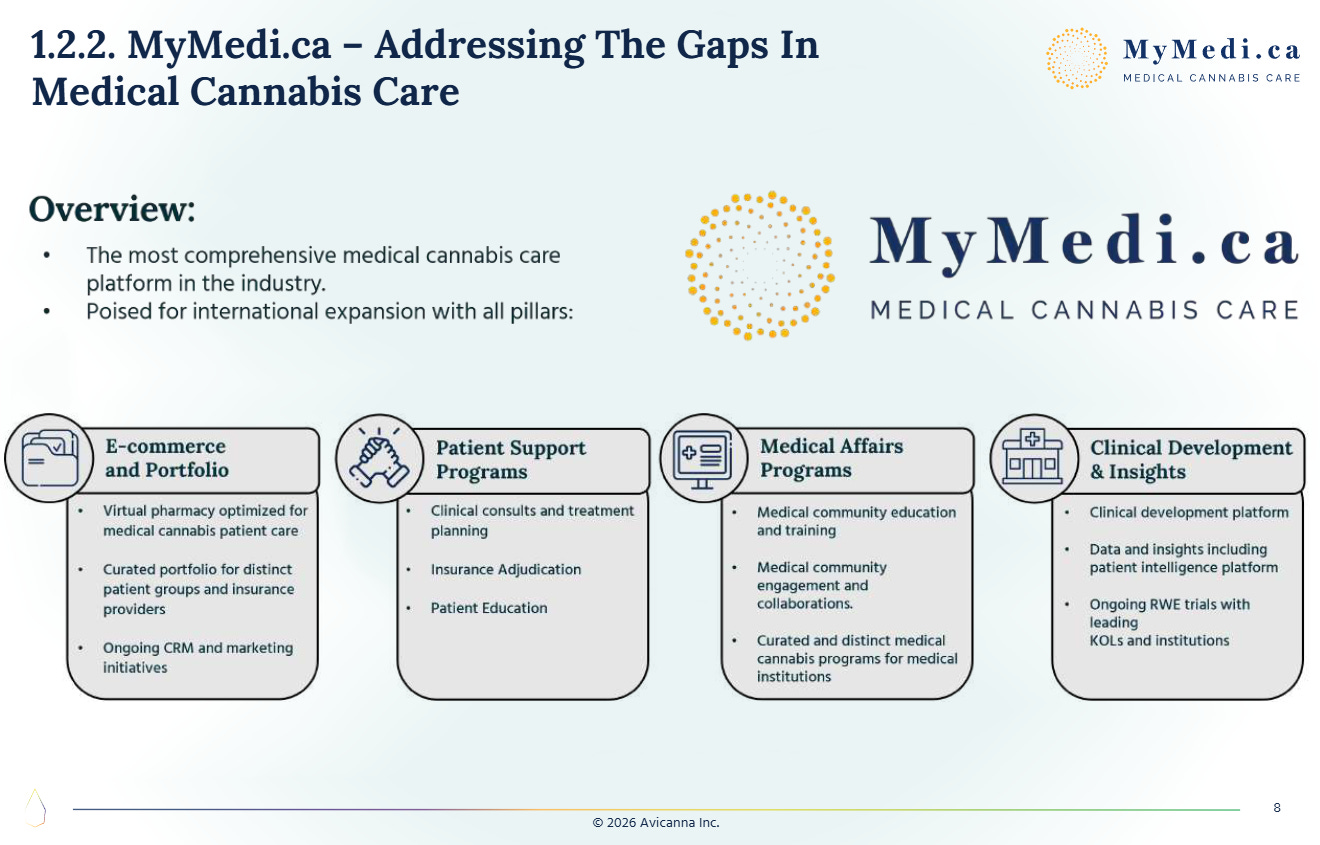

3. MyMedi.CA, a Canadian medical cannabis platform built around patients, physicians, pharmacists, education, and fulfillment

4. The pharmaceutical pipeline

Each of those can be looked at on its own. But the more interesting way to look at the company is through the way they connect.

Flower - Colombia and SMGH

The part that is most relevant to the investor framework above is SMGH, Avicanna’s Colombian subsidiary.

For years, cannabis investors and operators have talked about supply from places like Colombia or Thailand as a looming threat. The logic is obvious. Better climate. Lower labor costs. Year round cultivation. Export potential.

That threat is real. And any serious long term cannabis thesis has to account for it.

But what if it is not only a threat.

What if it is also investable.

Avicanna already has a majority owned Colombian platform through SMGH, partnered with Grupo Daabon, one of the largest organic agriculture companies globally, and SMGH is beginning to export organic GACP flower from one of the most optimal climates and lowest cost environments in the world.

That matters for two reasons.

First, low cost flower for export into medical markets is not theoretical. It is coming, and as it scales, it should put pressure on higher cost producers elsewhere.

Second, if that future is coming, then owning a stake in a credible low cost supplier is one way to participate in it rather than simply fear it. It can even function as a hedge in my portfolio against higher cost operators.

Credibility

This is where credibility starts to matter.

My impression is that Aras Azadian and his team have built real respect across the global cannabis ecosystem. They are taken seriously for their scientific approach, their formulation work, and their dogged persistence through difficult capital markets. That credibility should matter if the goal is to supply serious counterparties who need consistent, compliant, low cost, high-quality inputs. Having Grupo Daabon as a partner on the ground, provides further comfort and scalability.

I have heard Aras Azadian discuss cultivation costs in the range of $0.10 to $0.25 per gram. Yes, they grow biomass there too, but I am talking about beautiful sun-grown, organic and GACP certified flower for export at the same sort of cost per gram that would normally be associated with growing biomass.

There is a common assumption that outdoor/hoop house flower is inherently inferior, but it is also understood that the best sun-grown flower is among the best flower. SMGH appears positioned to take advantage of that dynamic, with the opportunity over the next three to five years to scale meaningful volumes of medical-grade flower in one of the lowest-cost environments in the world. That creates the possibility of producing very high-quality flower at a fraction of the cost of even the most efficient greenhouse operations worldwide.

There appears to be a credible path to EU-GMP certification for flower and later, extracts, and many hectares are available for potential expansion.

Perhaps most importantly, this is not a “build it and hope demand shows up” situation. Despite its small market cap, Avicanna already has credibility across the global cannabis ecosystem. The company and its CEO have established relationships with large operators and other serious counterparties, which should matter when thinking about how new supply actually gets placed into medical channels. That existing network and credibility base creates a very different starting point for scaling exports.

Still, this is only a small part of the Avicanna story.

What Medical Actually Means

Today, when companies, particularly in Canada, talk about their growth in medical cannabis export revenue, a large portion of what they are really talking about is the export of unbranded, bulk flower into markets like Germany (well, primarily Germany). That has been a meaningful release valve for the Canadian ecosystem. It has allowed operators to sell product without excise tax and, in many cases, at prices that are higher than what they can achieve domestically. It has, in effect, helped stabilize a number of cultivation businesses that would otherwise be far more challenged.

But it does not strike me as a durable end state.

As more supply comes online globally, margins on bulk flower should compress. That does not eliminate the category. It makes cost decisive.

In a more commodified world, the lowest cost, clean compliant producers set the floor for the system.

But if medical simply becomes a market for higher standard flower, then it is still largely an agricultural business, just with tighter rules.

That is why I think the medical conversation often stops too early.

Where Avicanna Is Different

The more interesting part of medical, longer term, is not the flower.

It is what sits on top of the flower.

It is formulation. Drug delivery. Clinical integration. Patient support. Education. Prescriber relationships. Data. Iteration.

This is where Avicanna stands out to me.

Yes, it has the Colombian platform.

Yes, it is developing what I would argue is among the lowest-cost, cleanest sources of supply being built for global medical markets.

Yes, it has scale potential and a credible path toward EU-GMP.

But, the real story of Avicanna, has less to do with Colombia and more to do with the value of the foundation they have erected over ten years of building and survival.

CEO Azadian describes medical cannabis as a service, not a product

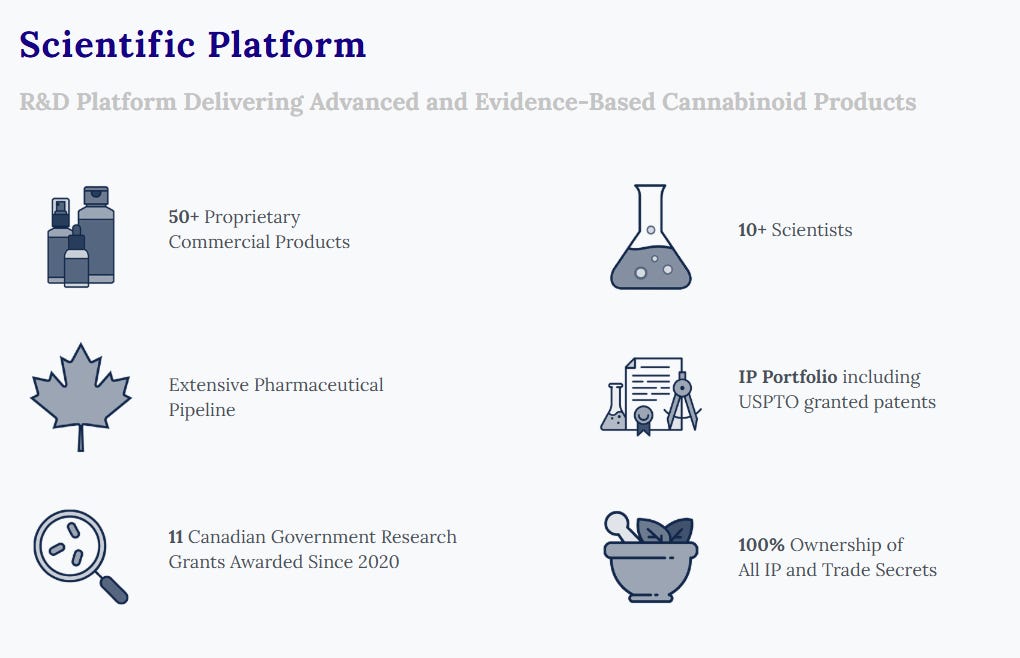

Over the past decade, Avicanna has built and commercialized a portfolio of proprietary medical cannabis formulations.

Those formulations are supported by a broader system that includes treatment planning, clinical guidelines, physician education, pharmacist interaction, patient support, and ongoing iteration through real-world use. This system feeds back into product development, iteration, and enables low cost clinical development.

That’s what MyMedi.CA and Rho Phyto, together, represent.

It’s not just a distribution channel with a line of generic medical cannabis products.

It’s infrastructure and proprietary intellectual property built around formulation, delivery, and repeatable medical use.

Putting it Together

This is why I think the investor’s framework, while directionally right, is incomplete.

He seems focused from my perspective on what will ultimately be the more commodity pieces of the cannabis business.

This will include:

Clean supply.

Low cost.

Consistency.

All of which matter.

But the long-term value in a medical market will not be created at the level of bulk input IMO.

It will be created at the level of formulation, drug delivery, clinical integration and probably brand.

And that’s exactly where Avicanna is building.

So instead of choosing between low-cost supply and higher-value medical products, the company is doing both.

Low-cost, compliant, scalable input from Colombia.

Paired with proprietary formulations, medical products, and infrastructure built over years in Canada.

That combination is where this starts to look very different from any other company I have come across in the world. This model with emphasis on IP is scalable and easily transferable to new markets with distinct regulations as Avicanna is not the finished product manufacturer.

The margins in the part of the medical market that looks like bulk flower will likely compress over time. There may be a window where high-quality extracts demand significant premiums on global markets, but this too will compress over time.

The part that looks like formulation, delivery, infrastructure and probably brand is where the long-term value sits because that is where gross margins can be best protected and defended.

MyMedi.CA

Avicanna took over MyMedi.CA, the former Shoppers Drug Mart medical cannabis business in 2023 and have been busy improving operations, rebuilding the assortment, cutting costs and preparing it for growth. For MyMedi.CA, “marketing” is achieved through education/medical affairs which require investment capital which has been scarce.

It seems to me there is an opportunity to the extent Colombia begins to spin off cash in 2026 and 2027 for the company to reinvest some of that into medical affairs which should help growth at MyMedi.CA (the largest piece of their present revenue base).

From my understanding, Avicanna’s approach to education/medical affairs is pretty unique in the industry, globally, and will be important if medical cannabis is going to truly take hold beyond flower.

Rho Phyto

Rho Phyto and other proprietary Avicanna brands have been increasing their already strong penetration of MyMedi.CA sales, but the company has also had success expanding proprietary Avicanna SKUs onto some of the other medical platforms in Canada and this continues to be a near term opportunity.

From my perspective, the company has another large, untapped opportunity in the Canadian rec market as well. This is presently too capital intensive and also a lower priority opportunity for a capital-starved, medically focused company, such as Avicanna, but that does not diminish my belief in it as a future opportunity for the company in Canada and globally.

More immediately, however, it seems like there may be a separate opportunity for the company to earn licensing fees in the Canadian rec market. The CEO has spoken of an “Intel inside”-like technology licensing model. It is my belief that Avicanna has some world class, proprietary, patented cannabinoid – related technology, but really, what the fuck do I know?

If we see, for example, another large Canadian, licensed producer or other serious cannabis operator globally license some of Avicanna’s technology and or finished products, that would seem like some helpful confirmation for my credence.

Only time will tell on this issue, but I see it as another big opportunity for the company and potentially a public validation of what they have been doing that would seem to me to be quite significant.

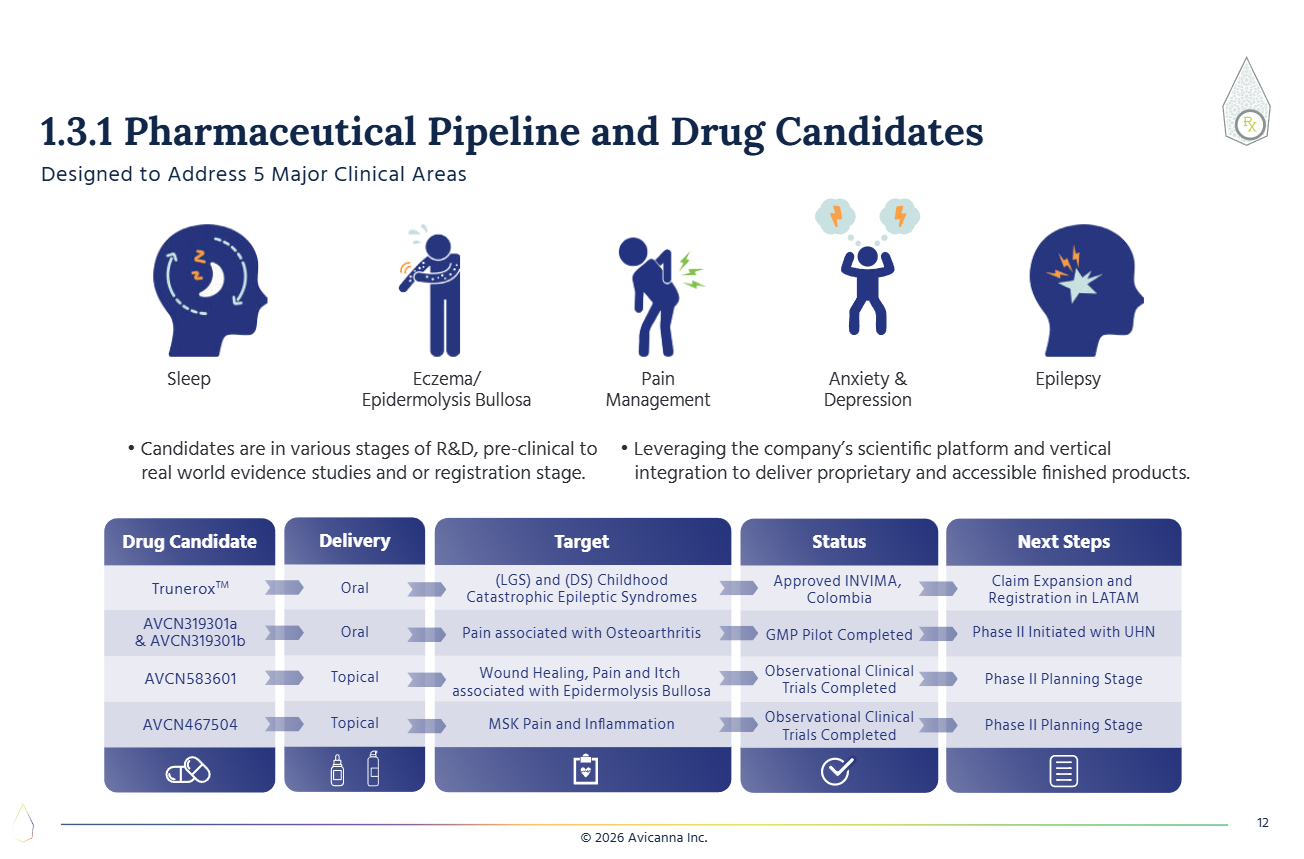

Pharmaceutical Pipeline

From my perspective, there are many ways to win with Avicanna in the short term and the medium and longer term, but there is also grand-slam-home-run potential if it can prove it’s medical-cannabis-intellectual-property-to-pharma-pathway successful, even just once.

This seems like more of a longer term opportunity, but one never knows when as there are already several drugs in their pipeline. Their existing and future pharmaceutical drug pipeline is informed by their product iteration, prescription and real world evidence trials with major academic and clinical institutions. It gives them an advantage in focusing on the most effective formulation/delivery mechanism, as well as targeting trials toward specific conditions that might have an easier road toward eventual FDA, etc. approval.

I don’t have much sense of how a traditional biotech/pharma analyst might value such potential, but I don’t expect much credit in the foreseeable future for this piece of the business (absent some mania - which is certainly possible).

Biotech companies normally spend lots of money on drug development, but Avicanna has not had that luxury. Avicanna has been advantaged by the Canadian regulatory landscape, which has allowed for this kind of R&D, and they have been able to conduct 10 years of development at lower cost due to the known safety profiles of the molecules and Avicanna’s scientific platform. That platform has included in-house R&D capabilities, in addition to academic and clinical institutions, and, with the support of government grants, has allowed for lower-cost development. Their expectation has been that they would bring in partners to fund further pharmaceutical-level clinical development. The pipeline is not really far enough along for us to understand any potential value from the outside, as far as I can gather.

So what happened here?

Why is this stock trading at a US$15 million market cap?

The answer from my perspective is a perfect storm inside a perfect storm.

The first perfect storm, was the last four years in the bust cycle of the cannabis industry. Like many other cannabis companies, this one was overvalued after its IPO when it was perhaps more like an idea on a napkin compared to the nearly-profitable-revenue-generating-IP-factory that it has developed into (even though the stock has essentially gone down ever since).

The stock was once over C$7 and was recently trading at C¢0.17.

I discovered this company only around one year ago, but I’ve been trying to piece together the history. The company attracted a short list of investors with large stakes, various combinations of whom, patiently helped the company stay funded over these many difficult years with targeted equity offerings to fund ongoing funding needs. From my perspective, this was done, responsibly and out of necessity with the most recent (and hopefully the last?) of these offerings happening on 2/10/2026 at $.20 per share, /which was a modest premium to the closing price on that date.

The challenge with a small market cap held tightly is that if one shareholder wants to sell or reduce her position, the physics of the situation can be quite difficult here, near the bottom of an extended cannabis industry bear market in a tightly held, illiquid, tiny microcap.

The largest shareholder of Avicanna has been selling the stock fairly aggressively and relentlessly for much of the last year as far as I can piece together from filings. In my parlance, these ongoing sales are the perfect storm inside the perfect storm.

I have no insight into whether another 10 million shares is going to come for sale or not, but my impression is that stock price drives narrative which is part of why I suspect there will be a lot more interest in this stock at $.50 than there is down here at $0.17.

This company is positioned too perfectly for the global industry context that I see for it to stay down here for too long. Avicanna’s moment is almost here.

---

My previous Avicanna Substack posts:

(6/11/25) https://markemerritt.substack.com/p/avicanna-a-pharmaceutical-approach

(7/25/2025) https://markemerritt.substack.com/p/cannabis-the-endocannabinoid-system

(12/25/25) https://markemerritt.substack.com/p/canadian-cannabis-some-updated-thoughts

Hi Mark, this is no doubt a very well thought out, sophisticated investment thesis and I have a tracking position myself, which I took mainly being inspired by your research. The main reason why the stock is drifting is most likely that there’s been practically no sales growth for several quarters now. Until some of the many inherent advantages that the company has translate into reignited top line growth, this may continue to be a sleeper. But when/if it does, the rerating could be dramatic.